Latest SEC Proposal Broker Conflict of Interest Causes More Than Confusion. Anyone Surprised?!

It would only seem logical that, after counting the thousands of instances (which are only partially revealed via Finra’s brokercheck database) in which retail investors have been ripped-off by licensed investment brokers who have sold an investment product without disclosing conflicts of interest courtesy of incentive fees or kickbacks those brokers are making from third parties when selling seemingly simple and/or complex investment products to the respective customers. After all, the burden of establishing rules of the road and regulating the practice of selling investment instruments has long been the domain of the US Securities & Exchange Commission and secondarily on Finra, which is a self-regulated body that governs the broker-dealer space–which is comprised of the universe of brokers who sell investment products. The SEC mandate–according to altruists–is to protect investors from abusive practices advanced by those selling investment products by establishing regulations that protect investors. Further, Finra’s mandate is to impose standards of compliance and to police broker-dealers to ensure they comport with SEC regulations.

Aside from the last comments being somewhat redundant, all of this would seem to make sense, were it not for the fact that Finra is the SEC’s biggest lobbyist. Finra member firms (who pay membership fees) are comprised of all of the brokerages that sell investment products to retail investors and by default, Finra is therefore conflicted when having the biggest lobbying influence on the SEC as to the rules and regulations that govern those member firms.

Sponsored by Prospectus.com. Our team of capital markets experts and securities lawyers specialize in preliminary offering prospectus, secondary offering prospectus and full menu of financial offering memorandum document preparation. More information via this link

Mr. Trump and Mr. Clayton (SEC Commissioner)

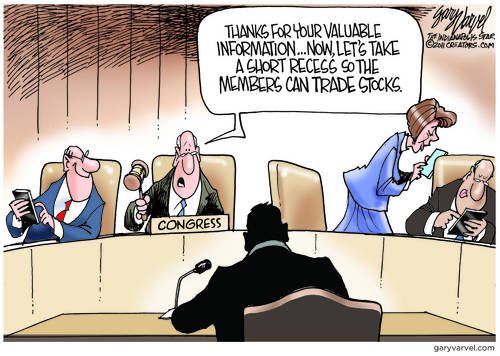

Yes, there are consumer advocacy groups that lobby the SEC to ensure proper protections are in place for unwitting investors. But, the fact is those advocacy groups do not have anywhere near the resources to effectively influence the handful of SEC Commissioners who are handpicked by the prevailing administration–meaning those sitting inside the White House. All one has to do is consider the circuitous path aggrieved investors must take when they’ve been wronged to realize the system is stacked against them, starting with investors having to bring their claims via an industry arbitration forum and foregoing their rights to sue the wrong-doers in an actual court of law. Once in arbitration, investors then face a forum that is typically overweighted with “expert” industry professionals–the folks who work for Finra member firms, whether as consultants or direct employees. More important, all one has to do is analyze the number of cases brought by investors against a member firm and their respective broker to recognize the cases resolved in favor of the investor are dwarfed by the number of instances in which a ‘no harm no foul’ determination is made in favor of the defendant.

The good news is that in recent years, enough outcry on the part of investors has led to among other things, the federal government establishing an independent watchdog in the form of the Consumer Financial Protection Bureau, whose role “is to make consumer financial markets work for consumers, responsible providers, and the economy as a whole. We protect consumers from unfair, deceptive, or abusive practices and take action against companies that break the law.” Further, thanks to prior White House administration, the SEC adopted a new set of standards intended to better protect the investor from their investment brokers and imposing guidelines that called for greater transparency and more granular disclosure as to conflicts of interest on the part of investment brokers so that investors could fully understand exactly where their investment dollars were directed and the actual returns on investment they could anticipate receiving.

The bad news is that Finra has fought with tooth and nail to water down those regulations and much like the NRA, they’re experts at navigating the swamplands of Washington DC. Further bad news-the Trump Administration’s doctrine to loosen regulations on banks and brokers with the goal of making it less onerous insofar as compliance overhead and regulatory oversight so banks can make big profits on transactions and enable them to be more leveraged has also taken aim at those pesky conflict of interest disclosure requirements imposed on investment brokers.

Before TrumpWorld (the political version of WestWorld), it was acknowledged that brokers should be disclosing fees they earn, including commission being charged to the customer and incentive fees the broker is getting paid from the manufacturer of the investment product.

But we know that Trumpeteers have long campaigned to turn the clock back and with the influence of the orange-haired guy sitting in the Oval Office, to bring the world back to the 1950′s so that business titans and US-styled oligarchs who play golf at Mar-A-Lago could become fatter cats than they already are. And that mindset has included the investment broker space, as evidenced by Trump’s SEC latest proposal to water down existing rules and pending legislation that would favor investors as opposed to the brokers selling investment products–who after all-are either country club members or who vie to be. That’s what makes America great, right?

Something funny happened after the SEC’s latest proposal-investors and brokers have balked. Here’s the opening excerpt from the WSJ coverage..

SEC’s Proposed Curbs on Stockbroker Advice Under Attack

Plan from Trump-appointed officials at SEC runs into criticism from both brokers, investors

WASHINGTON—A government proposal to restrict incentives that can bias broker advice to clients is generating complaints both from Wall Street and investor advocates.

The plan by the Securities and Exchange Commission, developed by Trump-appointed officials, may replace some aspects of an Obama-era regulation by the Labor Department that Wall Street successfully challenged in court. A federal court invalidated the Labor rule, and the Trump administration declined to appeal the decision, killing it for good.

Now investor groups, brokerages and other business groups are taking shots at the SEC’s attempt to address brokers’ conflicts of interest, saying that it is too vague and won’t improve protections for investors. The commission must consider the comments before it can vote to implement the regulation, perhaps sometime in 2019.

The SEC proposal would require brokers to act in the best interest of clients, barring the picking of lackluster or unsuitable investments because they make more money for them or the brokerage firm.

Investor groups say the SEC’s proposed requirements are so ambiguous that they won’t change the status quo. Brokerage firms, meanwhile, complain the measure creates a new standard without telling them how their brokers might run afoul of it. They also complain it treats them more harshly than investment advisers, who have a fiduciary duty to put their clients’ needs first.

“This will only serve to harm the brokerage model and limit choice for those investors who prefer the brokerage advice model,” wrote the American Securities Association, whose members include Cowen Inc., Stifel Financial Corp. and LPL Financial Holdings Inc.

The SEC didn’t define “best interest” in its April proposal. It also didn’t explicitly state how brokers should “mitigate” conflicts of interest that can undermine their need to provide legitimate recommendations.

To read the full coverage, click here