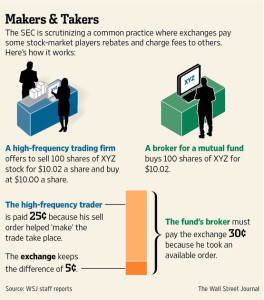

Exchange rebates paid to brokers for routing orders to their respective venues and the general issue with regard to the now ubiquitous “payment-for-order-flow” model that extends throughout the electronic trading ecosystem has been a topic of discussion for many years now. It may be confusing, but is certainly not an unknown concern to the universe of informed buy-side investors. For those who may be still be uninformed as to how/where/why/when (and how much?!) broker-dealers are on the receiving end of rebates, suffice to suggest its time you get yourself up to speed; your bottom-line can depend on it.

Image Courtesy of April 2014 Wall Street Journal

Courtesy of financial industry media outlet MarketsMedia’s all-star journalist Terry Flanagan most recent dissertation “Got Transparency?” it is one that deserves an accolade from altruists within the industry, if not a check under the hood or bottom of Terry’s car before he starts the engine.

“One aggravating factor is a lack of transparency. Many market participants do not know either the amount of the rebate or where it ends up.”

As Flanagan points out, “..In institutional equity trading, rebates have been a point of contention since the late 1990s, when Bill Clinton was U.S. President and the Dow Jones Industrial Average scaled 10,000 for the first time.

Supporters say exchanges paying rebates on order flow is a perfectly legitimate practice of rewarding customers and offering volume discounts. Helped by rebates, trading commissions have dropped substantially over the years; the biggest decline from 2005 to 2017 was 68% for the lowest-touch direct market access / algorithmic trades, according to Tabb Group research.

“Most buy-side firms operate with ‘all-in’ pricing models and aren’t provided granularity into fees by order, but the decisions on when and how to route to particular venues significantly impact execution performance…” according to Stino Milito, Co-Chief Operating Officer at Dash Financial Technologies.

On the other hand, critics say rebates create conflicts of interest, and shortchange end investors if brokers route in ways that disadvantages clients……Helped by rebates, trading commissions have dropped substantially over the years; the biggest decline from 2005 to 2017 was 68% for the lowest-touch direct market access / algorithmic trades, according to Tabb Group research.

“There is absolutely crap disclosure about broker-dealer routing strategies,” according to Dave Weisberger of ViableMkts. “If you can’t get a high-level view of how brokers route and what the outcomes are, then how can you be talking about a transaction fee pilot, or making claims about what rebates do to destroy the market?

Are you a startup fintech or blocktech firm that is seeking to raise capital and finding yourself ‘short of’ a cogent business plan or the proper investor offering documents?

Schedule your call with the senior executives at Prospectus.com LLCtoday

To read the entirety of Terry Flanagan’s piece in the latest edition of MarketsMedia, click here

The Great Rebate Debate..Broker Disclosure IS Front-Burner Topic

Latest SEC Proposal Broker Conflict of Interest Causes More Than Confusion. Anyone Surprised?!

It would only seem logical that, after counting the thousands of instances (which are only partially revealed via Finra’s brokercheck database) in which retail investors have been ripped-off by licensed investment brokers who have sold an investment product without disclosing conflicts of interest courtesy of incentive fees or kickbacks those brokers are making from third parties when selling seemingly simple and/or complex investment products to the respective customers. After all, the burden of establishing rules of the road and regulating the practice of selling investment instruments has long been the domain of the US Securities & Exchange Commission and secondarily on Finra, which is a self-regulated body that governs the broker-dealer space–which is comprised of the universe of brokers who sell investment products. The SEC mandate–according to altruists–is to protect investors from abusive practices advanced by those selling investment products by establishing regulations that protect investors. Further, Finra’s mandate is to impose standards of compliance and to police broker-dealers to ensure they comport with SEC regulations.

Aside from the last comments being somewhat redundant, all of this would seem to make sense, were it not for the fact that Finra is the SEC’s biggest lobbyist. Finra member firms (who pay membership fees) are comprised of all of the brokerages that sell investment products to retail investors and by default, Finra is therefore conflicted when having the biggest lobbying influence on the SEC as to the rules and regulations that govern those member firms.

Sponsored by Prospectus.com. Our team of capital markets experts and securities lawyers specialize in preliminary offering prospectus, secondary offering prospectus and full menu of financial offering memorandum document preparation. More information via this link

Mr. Trump and Mr. Clayton (SEC Commissioner)

Yes, there are consumer advocacy groups that lobby the SEC to ensure proper protections are in place for unwitting investors. But, the fact is those advocacy groups do not have anywhere near the resources to effectively influence the handful of SEC Commissioners who are handpicked by the prevailing administration–meaning those sitting inside the White House. All one has to do is consider the circuitous path aggrieved investors must take when they’ve been wronged to realize the system is stacked against them, starting with investors having to bring their claims via an industry arbitration forum and foregoing their rights to sue the wrong-doers in an actual court of law. Once in arbitration, investors then face a forum that is typically overweighted with “expert” industry professionals–the folks who work for Finra member firms, whether as consultants or direct employees. More important, all one has to do is analyze the number of cases brought by investors against a member firm and their respective broker to recognize the cases resolved in favor of the investor are dwarfed by the number of instances in which a ‘no harm no foul’ determination is made in favor of the defendant.

The good news is that in recent years, enough outcry on the part of investors has led to among other things, the federal government establishing an independent watchdog in the form of the Consumer Financial Protection Bureau, whose role “is to make consumer financial markets work for consumers, responsible providers, and the economy as a whole. We protect consumers from unfair, deceptive, or abusive practices and take action against companies that break the law.” Further, thanks to prior White House administration, the SEC adopted a new set of standards intended to better protect the investor from their investment brokers and imposing guidelines that called for greater transparency and more granular disclosure as to conflicts of interest on the part of investment brokers so that investors could fully understand exactly where their investment dollars were directed and the actual returns on investment they could anticipate receiving.

The bad news is that Finra has fought with tooth and nail to water down those regulations and much like the NRA, they’re experts at navigating the swamplands of Washington DC. Further bad news-the Trump Administration’s doctrine to loosen regulations on banks and brokers with the goal of making it less onerous insofar as compliance overhead and regulatory oversight so banks can make big profits on transactions and enable them to be more leveraged has also taken aim at those pesky conflict of interest disclosure requirements imposed on investment brokers.

Before TrumpWorld (the political version of WestWorld), it was acknowledged that brokers should be disclosing fees they earn, including commission being charged to the customer and incentive fees the broker is getting paid from the manufacturer of the investment product.

But we know that Trumpeteers have long campaigned to turn the clock back and with the influence of the orange-haired guy sitting in the Oval Office, to bring the world back to the 1950′s so that business titans and US-styled oligarchs who play golf at Mar-A-Lago could become fatter cats than they already are. And that mindset has included the investment broker space, as evidenced by Trump’s SEC latest proposal to water down existing rules and pending legislation that would favor investors as opposed to the brokers selling investment products–who after all-are either country club members or who vie to be. That’s what makes America great, right?

Something funny happened after the SEC’s latest proposal-investors and brokers have balked. Here’s the opening excerpt from the WSJ coverage..

SEC’s Proposed Curbs on Stockbroker Advice Under Attack

Plan from Trump-appointed officials at SEC runs into criticism from both brokers, investors

By

Dave Michaels

WASHINGTON—A government proposal to restrict incentives that can bias broker advice to clients is generating complaints both from Wall Street and investor advocates.

The plan by the Securities and Exchange Commission, developed by Trump-appointed officials, may replace some aspects of an Obama-era regulation by the Labor Department that Wall Street successfully challenged in court. A federal court invalidated the Labor rule, and the Trump administration declined to appeal the decision, killing it for good.

Now investor groups, brokerages and other business groups are taking shots at the SEC’s attempt to address brokers’ conflicts of interest, saying that it is too vague and won’t improve protections for investors. The commission must consider the comments before it can vote to implement the regulation, perhaps sometime in 2019.

The SEC proposal would require brokers to act in the best interest of clients, barring the picking of lackluster or unsuitable investments because they make more money for them or the brokerage firm.

Investor groups say the SEC’s proposed requirements are so ambiguous that they won’t change the status quo. Brokerage firms, meanwhile, complain the measure creates a new standard without telling them how their brokers might run afoul of it. They also complain it treats them more harshly than investment advisers, who have a fiduciary duty to put their clients’ needs first.

“This will only serve to harm the brokerage model and limit choice for those investors who prefer the brokerage advice model,” wrote the American Securities Association, whose members include Cowen Inc., Stifel Financial Corp. and LPL Financial Holdings Inc.

The SEC didn’t define “best interest” in its April proposal. It also didn’t explicitly state how brokers should “mitigate” conflicts of interest that can undermine their need to provide legitimate recommendations.

Now that crypto cool kids are finally getting the memo: “These are Securities!” , the proposed first fully regulated Securities Token Exchange is coming to the US-via the Boston Options Exchange.

tZERO, the digital-themed broker-dealer created by Patrick Byrne and BOX Digital Markets LLC (BOX Digital)-a subsidiary of Boston Options Exchange, announced it has formed a joint venture to launch the industry’s first regulated security token exchange.

Lisa Fall, Box Digital

On May 18, 2018, the two companies entered into a letter of intent to form an exchange to list and publicly trade security tokens for companies that issue, or convert existing stock to, security tokens. The proposed joint venture would be equally owned by tZERO and BOX Digital, with each having equal representation on the Board of Directors, together with one mutually agreed upon independent director. Lisa Fall, who currently serves as CEO of BOX Digital and as president of BOX Options Exchange LLC, would be the CEO of the joint venture.

“tZERO has proven to be a pioneer in the development and practical use of blockchain technologies for capital markets for a number of years,” said Ms. Fall. “tZERO’s track record and accomplishments in this innovative area, coupled with BOX’s expertise in operating a highly efficient and transparent equity options marketplace, made partnering together an easy decision and we look forward to building a world-class platform for listing and trading security tokens.”

tZERO plans to contribute cash and license tZERO’s blockchain technology for operation of the security token market. BOX Digital will contribute expertise and personnel toward obtaining regulatory approval and operation of the security token market. Approval of the U.S. Securities and Exchange Commission will be sought following execution of definitive documentation. Creation of the joint venture is subject to definitive documentation and customary conditions.

“Our partnership with BOX Digital Markets is a significant milestone that will create the first SEC-regulated exchange designed to efficiently trade crypto securities. Lisa Fall’s leadership, reputation and deep experience in the regulated securities exchange industry will be a major asset in achieving this objective,” said Saum Noursalehi, newly appointed CEO of tZERO. “Together, we will continue to work with the SEC as we develop a first-of-its-kind platform that will integrate blockchain capital markets into the current U.S. National Market System.”

“Now that pragmatic securities industry thought-leaders have figured out how to package crypto assets within the construct of a security so as to conform to the US regulatory regime, nobody can dispute the fact the genie is out of the bottle . Securities Token Offerings (“STOs”) is a much more palatable approach, making way for a new mantra, “ICOs are dead, long live STOs”, until of course, another shoe drops.

For the full story from Traders Magazine, click here

August 15 2017-A Special Editorial from BrokerDealer.com: Most Fortune CEOs, as well as leaders of Investment Banks and Broker-Dealers (aka BD) are typically loathe to take a political stand. For the former, making pronouncements that will raise the ire of the current president are likely to be met by “injury by twitter,” or worse still, federal agency scrutiny of the company, which could prove devastating for public company shareholders. For the universe of corporate leaders with a conscience and also recognized thought-leaders, only a few have yet to prove unequivocal when reacting to the equivocal comment made by President Trump when framing his first view of what US Attorney General Sessions labeled as a”domestic terror event.” We’re referring to the white supremacist rally that led to 3 deaths and multiple injuries in Charlottesville, VA this past weekend.

For investment banks and broker-dealers, let’s face it-politics and business mix best with each other when done over cocktails or discrete ‘off-site’ meetings to discuss new capital market initiatives, deal issuance and/or asset management mandates. After all, most traditional broker-dealers eschew taking a political stand that opposes the federal government administration, simply out of fear that the long lips of the current WH CEO will whisper to administration-appointed SEC bureaucrats with a message akin to ‘the right industry regulator might want to make this [firm] go away..” Most, but not all is the catchphrase that compels a re-distribution of a capital markets desk commentary that focuses on fixed income markets and along with a smidgen of geopolitical observations and delivered to a captive group of leading Fortune 500 corporate treasurers, as well as a select group of sell-side syndicate desk ‘book-runners’. Here’s the extract of the day’s piece, titled Risk On, Risk Off, US-NOKO Tensions Subside; Ugly Heads of Racism Take Top Headline…

Investment Grade Corporate Debt New Issue Re-Cap – A View About Charlottesville and the Aftermath

Risk was clearly back on in the financial markets today, as U.S./NOKO tensions fell to the wayside. Unfortunately prejudice and racism reared their ugly heads in the Charlottesville, Virginia riot over the weekend. On Monday, Fortune 500 thought leaders Ken Frazier, CEO of Merck & C0., Brian Krzanich, CEO of Intel, and Kevin Plank, CEO of Under Armour each took a stand by protesting the ‘equivocal’ comments made by President Trump in his first response to the domestic terrorism acts in Charlottesvile, which were advanced by self-proclaimed alt-right and white supremacist neo-Nazis. Our firm stands with every corporate executive who stays true to their own right-minded beliefs and their company’s dedication to doing right and doing good, many of whom also maintain proactive Diversity & Inclusion initiatives. For those corporate executives who spent all of their undergrad time in finance and accounting classes, and perhaps not as familiar with the history of the United States as they could be, racism and bigotry are diseases, and cancers that every generation of this country has been working to eradicate.

To the above point, one only need to re-read the Constitution and the Bill of Rights to appreciate that D&I is actually part of our country’s DNA. It is also part of the cultural foundation of many Fortune 500 corporations, including Intel, including Merck, including Under Armour and including many others! D&I means respect for and appreciation of differences in ethnicity, gender, age, national origin, disability, sexual orientation, education, and religion. But it’s more than this. We all bring with us diverse perspectives, work experiences, life styles and cultures and we presumably all share a disdain for anyone and any group that attempts to dismantle, disrupt and or destroy. Kudos to Mssrs. Frazier, Krzanich and Plank for putting themselves in harm’s way and risk of “injury by Twitter” for being true leaders and staying true to their convictions and their constituents. Kudos also to the many Fortune executives who have raised their own voices and to those who, like Jamie Dimon, have opted to protest by remaining that much more proactive in the WH-appointed roles in which they serve as volunteers.

Today’s VIX closed 3 bps tighter versus Friday’s close. Also a reminder that tomorrow is August 15th – “mid-August” – that’s when North Korea’s illustrious “bad boy” proclaimed that he’d have his master plan ready to bomb Guam developed by. One week from today on Monday, August 21st begin joint U.S-South Korean military exercises referred to as Ulchi-Freedom Guardian. The exercise began in our Bicentennial year of 1976. North Korea has annually perceived the joint exercise as “preparation for war.” It is the world’s largest computerized command control implementation. Up to 80,000 American and South Korean troops have participated in this exercise in the recent past. The game will go on for two weeks before concluding on Thursday August 31st. Enjoy the show Mr. Jong-Un. You’ll have front row seats though I recommend binoculars. Here’s lookin’ at you kid!

If you ask me this is the perfect time for corporations to issue bonds. Not a bad thing will really happen, risk is back on and summer vacations are quickly approaching. My prediction – expect Amazon to the hit the tapes first thing tomorrow morning. Free market enterprise at work. Ya gotta love it!

Today’s IG Corporate dollar DCM finished with 5 issuers that priced 7 tranches between them totaling $4.10b

Private Placement Offerings Surge as Demand for Offering Memorandum Document Experts Follows Along

Whether due to improving economic conditions in the US as well as various other parts of the world, or due to technology advancements that serve as the catalyst to innovative products and services that solve legacy business challenges, the global private placement marketplace is surging. With this new era of entrepreneurship, the need for investor offering memorandum experts is likewise cascading. In Wall Street parlance, the demand for such experts is nearly “over-subscribed,” meaning the supply of capable professionals who specialize in preparing fully-compliant investor offering documents is being stretched thin. But, at least one firm within the professional services sector is addressing the investor documentation needs of forward-thinking business enterprises and they are situated neatly within the “curl of the wave”-all you need to find them is a search engine and the right key words/phrases.

Operating under the web banner OfferingMemorandum.com, the firm behind this portal is NY-based Broker Dealer LLC and with footprints in various cities across the global financial services ecosystem, they are leading the pack by making it simple and easy for broker-dealers*, captive business advisors and corporate lawyers for companies of any size and located in nearly every geographic location of the world to engage local securities law professionals and investor offering document experts who specialize in preparing preliminary offering memorandums, red herrings and final offering prospectus documents that conform to financial industry best practices and comply with local regulatory guidelines that govern investor solicitations. (*For various reasons, registered broker-dealers do not prepare the investor offering memorandum or an offering prospectus, and it is therefore incumbent on the Issuer to provide the investor offering documents.)

Ryan Gorman, Prospectus.com

According to Ryan Gorman, a PR-IR-Corporate Communications expert who works with many startup companies, “While some capital markets professionals will attribute the continued spike in private placement issuance to the ‘Trump Bump”,others will credit the evolution of the JOBS Act [the US legislation spearheaded by former President Obama intended to make the regulatory steps more simple for small companies in the US to raise capital], global macro gurus point to the rising economic tides in various regions of the globe. That said, nobody disputes the number of new companies and latter-stage funding initiatives for small, medium and large companies remains in an unobstructed uptrend.

Private Placement offerings are surging and direct IPOs are gathering steam. But, for those seeking to raise capital for a start-up or to fuel expansion for a fast-growing business, any entrepreneur worth his salt knows their first step is preparing a cogent business plan, then consolidating that blueprint into a short-form ‘pitch deck’ and once prospective investors have expressed interest in the investment opportunity, the enterprise seeking capital (aka “Issuer”) provides the investor with an offering memorandum or an offering prospectus. Simple as this process might sound, offering memorandum preparation is non-trivial and is typically performed by securities attorneys who specialize in investor offering documents. Also known as an “OM”, the offering memorandum is perhaps the most critical document, as it frames the terms and conditions of the investment, and when prepared within the context of best practices, the offering memorandum is the document that both Issuer and Investor can hang their hats on. Somewhere in the mix, the enterprise that seeks funding (also known as the Issuer) might engage a registered broker-dealer to serve as a placement-agent aka underwriter for the financing round, or the Issuer may already have identified investors and has determined there is no need to engage a broker-dealer

*Registered broker-dealers generally serve as a placement agent or underwriter for a capital raise, but typically defer to the Issuer to provide them with the investor offering documents, as such it is the obligation of the Issuer or their corporate counsel to create an offering memorandum or a prospectus. In most instances the Issuer will engage their law firm to prepare these documents, and increasingly, law firms that do not have a securities law practice will outsource or sub-contract to firms that dedicated to this type of work. As the number of private placement offerings and direct IPOs via Regulation A+ continues to grow, portals such as OfferingMemorandum.com and Prospectus.com provide a unique solution.